Cash vs Accrual Accounting Explained: Pick the Right Method for Growth

Choosing how to record your income and expenses might not sound exciting, but picking the right accounting method can save your business serious time, money, and tax headaches. If you've ever wondered about the difference between cash and accrual accounting, you're not alone. Understanding how each method works and which one is best for your business is a critical step.

Let’s break it down clearly and simply, so you can make an informed decision with confidence.

What is an Accounting Method?

Your accounting method determines how and when you record your company’s financial transactions—like sales, invoices, and payments. There are two primary accounting methods you should know:

Cash accounting method

Accrual accounting method

Some businesses may use a hybrid method of accounting, but for most small business owners, you'll be choosing between cash and accrual accounting.

Cash Basis Accounting: Simple and Straightforward

What Is Cash Accounting?

Cash basis accounting tracks income and expenses when cash actually changes hands. That means:

You record income only when your business receives a payment.

You record an expense only when you actually pay the bill.

This method is especially common among small businesses, freelancers, and sole proprietors, largely because it's easy to manage and shows you how much cash the business really has (or doesn’t).

When to Use the Cash Method

The cash method of accounting could be right for your business if:

You're a small business with no need to track accounts receivable or accounts payable.

You want to focus on cash flow - that is, how much cash you have on hand.

Your company invoices rarely or operates mostly on immediate payments.

Many small businesses use the cash basis method because it is simple and provides a clear picture of cash flow without complicated forecasts.

Advantages of Cash Basis Accounting

Simple to understand and implement.

Focuses on actual money in your bank account.

Ideal for cash flow management.

No need to track invoices or bills until they're paid.

Things to Consider

Doesn’t reflect earned revenue or liabilities.

May lead to a misleading financial picture if many transactions are pending.

Not accepted under Generally Accepted Accounting Principles (GAAP), and public companies or businesses with inventory are typically required to use the accrual method.

That distinction is key. If your business needs to raise investment, carry goods as inventory, or plans to become a public company, you may be required to switch to accrual.

Accrual Accounting: The Big Picture Perspective

What Is Accrual Accounting?

Accrual accounting recognizes income when it is earned, and expenses when they are incurred - not when cash is received or paid.

Here’s how that works:

You send an invoice: It’s counted as revenue, even if your customer hasn’t paid yet.

You receive a bill: It’s recorded as an expense, even if you haven’t paid it.

Why Use the Accrual Method of Accounting?

Businesses use the accrual method of accounting to get a more comprehensive snapshot of financial health. While it doesn’t track cash on hand as precisely, it offers a better match between income and expenses - known as the matching principle.

Under this system, you’ll also get clear insights on:

Accounts receivable

Accounts payable

True profit or loss

Benefits of Accrual Accounting

Accrual accounting provides a more accurate picture of your company’s financial position.

Helps match revenue to the expenses that earned it.

Required under GAAP for larger companies.

More appealing to investors, lenders, and management teams.

Drawbacks to Consider

More complex bookkeeping.

Can make cash flow harder to track without good accounting software.

You may owe taxes on revenue before the money actually hits your bank account.

Because of this, many small business owners find themselves nervous about potentially paying tax on money they haven't yet collected.

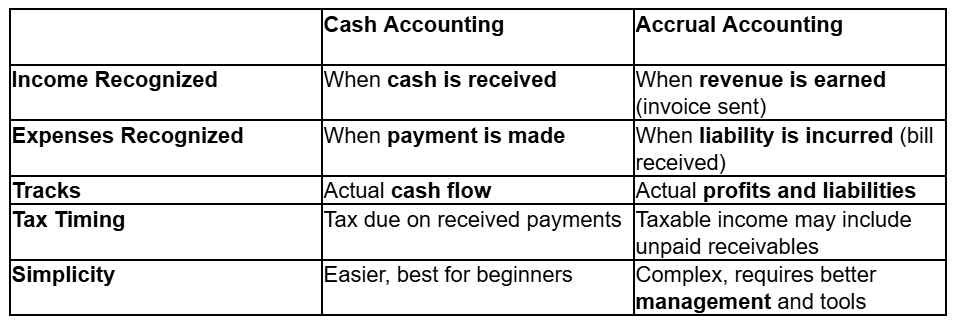

What’s the Difference Between Cash and Accrual Accounting?

The major difference between cash and accrual accounting lies in the timing of when income and expenses are recognized.

In a Nutshell

Cash-basis accounting is all about how much cash your business actually has.

Accrual-basis accounting gives a more thorough understanding of your company’s performance over time.

How Accrual Accounting Affects Your Taxes

It’s important to know that accrual accounting may increase your taxable income if you’ve invoiced customers but haven’t yet received payment. The IRS will still count it as income.

That’s why accrual accounting affects your taxes - often in unexpected ways. Depending on your fiscal year-end, invoicing in December could mean tax liabilities before getting paid in January.

Generally:

Businesses making over $27 million in average gross receipts typically must use the accrual method.

If you hold inventory, you may be required to use accrual accounting.

Which Method is Right for Your Business?

Choosing between cash or accrual accounting often comes down to the size of your business, its complexity, and your growth expectations.

Choose Cash If You:

Run a service-based business without inventory.

Operate on a small scale.

Want simple bookkeeping aligned with your cash flow statement.

Need to closely manage cash on hand.

Choose Accrual If You:

Sell products and track inventory or cost of goods sold.

Want to match sales and expenses within the same fiscal year.

Plan to grow, attract investors, or apply for credit with a bank.

Want financial statements aligned with Generally Accepted Accounting Principles.

You might also find benefit from consulting with a Certified Public Accountant (CPA) who can review your financial statements and determine what’s best for your situation.

Transitioning or Switching Methods

If you’re already using the cash basis and want to switch to accrual, you’ll need IRS approval - especially if it results in a taxable income change. The method you choose also affects:

How you recognize deferred revenue or deferral of expenses

Adjustments to depreciation

Reporting methods on your income statement and balance sheet

If you're still unsure which accounting method to use, working with professionals like our local Denver bookkeeping services can help keep your books compliant and optimized for decision-making.

The Role of Accounting Software

No matter which method you use - cash or accrual accounting - good accounting software makes things infinitely easier. Tools like QuickBooks allow you to toggle between cash-basis accounting vs accrual-basis accounting inside your reports.

This helps:

Automate financial transactions

Track invoices, payments, and expenses

Generate real-time financial statements

Forecast cash flow

Just be sure your software aligns with your chosen basis of accounting and complies with accounting principles and IRS regulations.

Final Thoughts: Getting Accounting Right from the Start

So, what's the difference between accrual and cash accounting really about? Timing.

Cash method = account for income/expenses when money moves.

Accrual method = account for them as they happen, regardless of when cash changes hands.

Your goal as a business owner isn’t just to stay organized—it’s to position your company for sustained growth, tax efficiency, and financial clarity.

The accounting method you pick impacts everything: your profit, your investment readiness, your year-end tax bill, and your peace of mind.

Next Steps

If you're a small business just getting started, and you want to use cash accounting, that's often a fine place to begin.

If you're growing fast or working with customers who take time to pay, use the accrual method for a more accurate snapshot.

Still not sure what’s best for your business? Reach out to our Denver bookkeeping services team and get peace of mind knowing your accounts are in expert hands.

The cash vs accrual accounting debate only matters if it’s helping you run a better business—so choose the system that keeps you informed, compliant, and confident.

Let us help you turn those numbers into knowledge.