How Many Years of Financial Records Should I Keep? Find Out What to Save

If you've ever stood in front of an overflowing file cabinet wondering what to toss or keep, you're not alone. One of the most common personal financial planning questions we hear is: How many years of financial records should I keep?

The truth is, it depends on the type of document, what it’s used for, and whether it’s needed for legal, personal, or IRS-related reasons. Below, we’ll walk you through what to keep, what to shred, and how to confidently organize your financial life here in Denver, Colorado.

How Long Should You Keep Financial Records?

Let’s start with the basics: there isn’t a one-size-fits-all approach to record retention. Some documents need to be saved for just a few months, while others should be kept indefinitely.

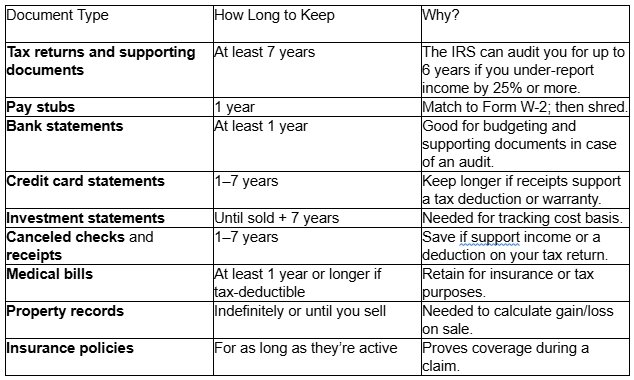

Here’s a simple breakdown of how long you should keep common financial documents:

Keep Tax Records the IRS Might Ask For

The IRS recommends keeping tax documents for three to seven years, depending on the situation. The general rule of thumb is:

Keep documents that support a deduction on your tax return for as long as possible.

The IRS can audit your return three years after filing.

If they suspect fraud or underreporting income, they can audit you for up to six years.

No limit applies in cases of fraud, so in rare circumstances, keeping indefinitely may apply.

For a more detailed look, the IRS offers retention guidelines that you can review here.

Which Paper Documents and Legal Documents to Keep and For How Long?

Many legal and financial documents are hard to replace and should be kept either long-term or forever.

Documents to Keep Indefinitely

Birth certificates, Social Security cards, and passports

Marriage licenses/divorce decrees

Legal documents related to inheritance or court judgments

Property records

Wills, trusts, and powers of attorney

These should be stored safely in a home safe or a bank safe deposit box. It’s also smart to keep records electronically as a backup.

Keep and Shred: What You Can Toss and When

Once you’ve reviewed the retention guidelines, it’s time to start sorting.

You’ll want to shred documents such as:

Old credit card bills no longer needed

Bank statements older than one year (if not needed for tax purposes)

Expired warranties

Paid utility bills, unless used as proof of expense

Use a paper shredder to protect your personal information from identity theft.

Keep Financial Records That Support Your Situation

Your personal situation might require longer retention. If you’re self-employed, own rental property, claim frequent deductions, or make large charitable donations, you’ll need to be more meticulous.

Records to pay special attention to include:

Receipts for donations or large purchases

Receipts and checks supporting a charity deduction

Financial statements related to stock or asset sales

Tuition payments and student loan documents for education tax credits

Mortgage payment records for loan interest deductions

Anything needed for tax purposes

Why You Need to Keep Documents for Tax Purposes and Beyond

Tax-related record keeping isn’t just about surviving an audit. Organizing documents also supports smarter financial planning and gives you peace of mind during emergencies or major life events.

Here's why it matters:

Tax advisors need complete information for optimized returns and deductions.

The IRS may request documentation years after an income tax return is filed.

Well-kept financial records help prevent fraud and simplify records management.

Knowing what to save spares you from hunting down original documents or making costly errors.

Digital vs. Physical: Should You Save Records Electronically?

If space is tight in your drawer or filing cabinet, or you’re tired of managing loose paper, storing records digitally can be a great solution.

Here’s what you can do:

Scan documents that support federal tax deductions using a secure backup system or file-hosting service

Use strong password protection on all files

Save extra copies in a cloud-based directory and an external hard drive

Follow strict privacy and security policies to avoid compromising personal documents

Just make sure scanned docs are legible and organized by year or category. This method works well for records that support your tax return and payment history.

When In Doubt, Ask a Professional

If you're still not sure how long to keep financial records or exactly what you can shred, get expert help. A seasoned tax accountant in Denver can review your paperwork and tailor a plan that fits your financial goals, tax situation, and Denver’s local policies.

Final Thoughts: Be Smart with Record Keeping

Organizing your financial documents isn’t just about avoiding clutter - it’s about building confidence for whatever life throws at you. Whether you're managing the documents after your first financial year or decluttering after decades, these record retention guidelines can help

To recap:

Keep most tax documents, supporting documents, and paper documents for at least seven years

Store legal and financial documents indefinitely

Shred anything that contains personal financial data you no longer need

Use electronic storage with backups for convenience and safety

Start with what you can handle now: toss what’s safe, protect what matters, and when in doubt, reach out for solid financial advice.